What is the Role of Blockchain in Digital Banking and Payments?

Category : Blockchain / by Andrew

Blockchain technology, which first emerged through the cryptocurrency Bitcoin, faced scepticism at first. However, as the technology evolved, it presented its unusual features of decentralisation, immutability, transparency, and security, which no other technology had offered so far. These innovative capabilities sparked curiosity across various industries, particularly banking, which started exploring Blockchain Development to fully capitalise on its potential and solve existing challenges. In recent years, blockchain adoption in banking has progressed considerably, bringing sophisticated solutions to digital payments and financial transactions. Let’s go into greater detail about the role of blockchain technology in digital banking and payments.

Why does the Banking Industry Need Blockchain Technology?

Most banking institutions use standard centralised systems to manage their workflow, including verifying user identities, processing payments, and managing user accounts, among other complex operations. The traditional banking systems have been used for ages, but presented several challenges, including:

- Centralised data storage is vulnerable to fraud and other risks such as identity theft, money laundering, and cyberattacks.

- Banking networks involve multiple intermediaries, such as correspondent banks, clearinghouses, and more. It adds up both the operational value and the service charges for the customers.

- Bank payments, especially international money transfers, can take several days to reach their intended recipient. These delays are common due to banking holidays, time zone differences, complex verification criteria, etc.

- The complexity of banking networks prevents transparency. It makes it difficult for banks to provide insights into transaction flows to both customers and regulators.

- Every day, banks dedicate significant resources to reconciling accounts, updating accounting records, and ensuring accuracy across multiple systems.

How Is Blockchain Transforming Digital Banking and Payments?

As is evident, the banking sector has a lot to deal with, which created the need to adopt blockchain software development. But what does this technology actually mean, and how does it work in banking?

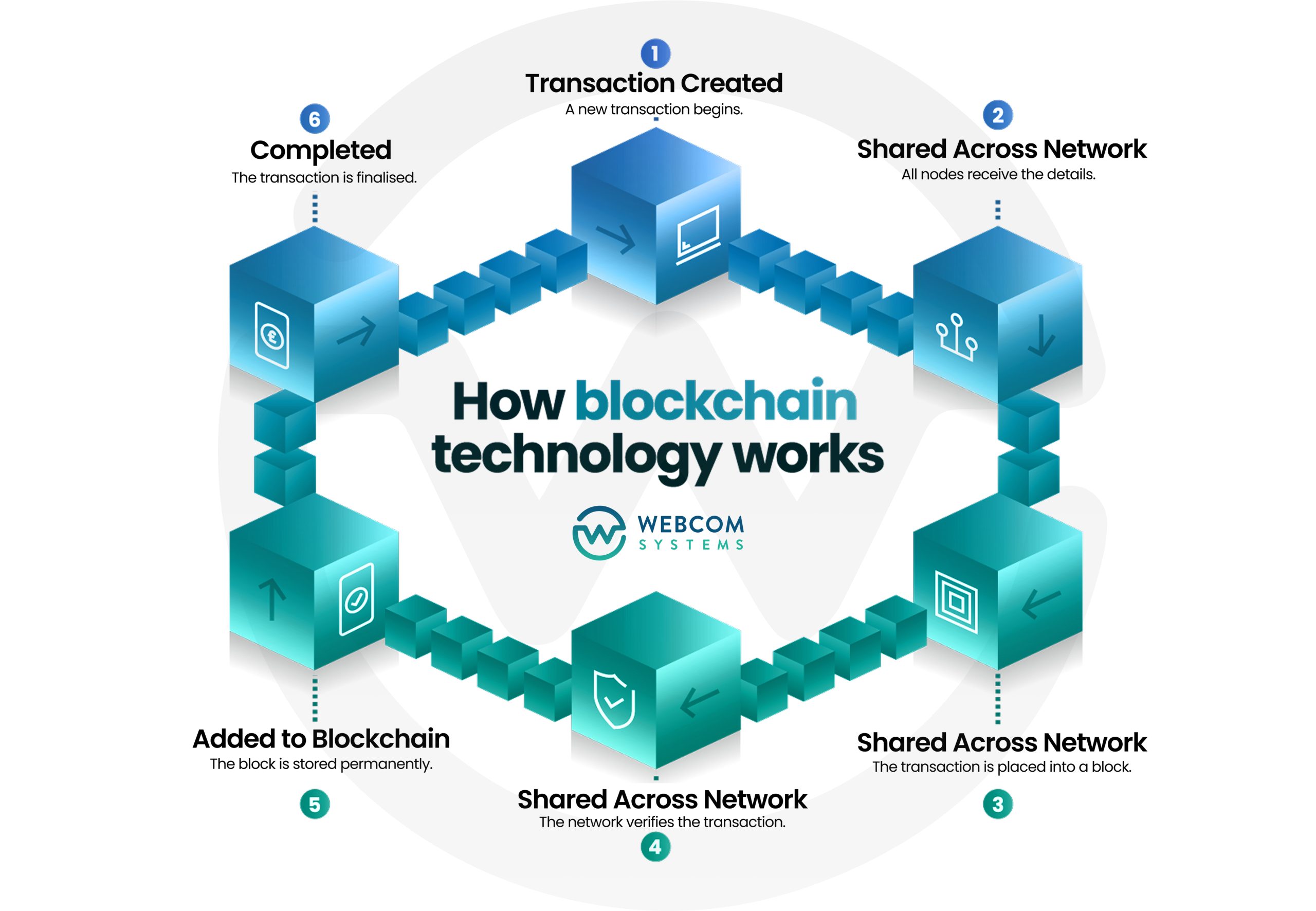

Basically, Blockchain technology is a distributed system that records transactions across a network of computers. Hence, it is also called decentralised ledger technology. All the transactions stored on its “shared” ledger are secure, transparent, and immutable to deletion or any kind of alteration.

A blockchain network consists of numerous participants and facilitates peer-to-peer transactions. Unlike traditional business databases, no single entity holds the centralised or full control.

When a transaction occurs on a blockchain network, it is broadcast to all participants. Furthermore, these network participants validate the data and store it as a ‘block’. These blocks are then linked together to form a chain that cannot be altered, ensuring immutability while providing transparency and reliability. Additionally, since every participant holds a copy of the chain, the cryptographic architecture is highly resistant to hacks.

When a transaction occurs on a blockchain network, it is broadcast to all participants. Furthermore, these network participants validate the data and store it as a ‘block’. These blocks are then linked together to form a chain that cannot be altered, ensuring immutability while providing transparency and reliability. Additionally, since every participant holds a copy of the chain, the cryptographic architecture is highly resistant to hacks.

Hence, this decentralised record-keeping is employed in banking and finance to offer safe, transparent, and quick digital banking and payments. Here are some of the benefits of adopting blockchain development technology in the banking sector:

Key Benefits Of Blockchain In Digital Banking

- Security and Fraud Prevention

Blockchain utilises a cryptographic framework to record data and is resistant to data manipulation. Once added to the chain, the block attaches permanently and becomes an unalterable part of the record. It reduces the risk of fraud or unauthorised access and hence secures banking operations.

- Quicker Digital Payments

As the blockchain enables peer-to-peer transfers, it removes the need to involve multiple intermediaries for processing payments. As a result, transactions are processed much faster and at a lower cost. Thus, benefits both the banking institutions as well as customers.

- Transparency and Traceability

Blockchain’s distributed ledger records each transaction in a chronological order, which only the authorised participants can access. This provides complete transparency, easy traceability, and reliable auditability across the network. Hence, improving accountability in the banking ecosystem.

- Reduced Operational Costs

Banks can reduce operational costs by using the blockchain’s distributed ledger, which eliminates the need for manual record-keeping and extensive paperwork. Moreover, smart contracts can automate most operational tasks and even reduce human errors.

Also Read: A Complete Guide to the Top Blockchain Development Tech Stacks

Blockchain Applications in Digital Banking and Payments

There are multiple applications of blockchain development in improving digital banking and payments, as mentioned below:

- International Payments with Blockchain Platforms

Traditional cross-border payment systems rely on multiple banking networks (SWIFT network) and intermediaries, making transactions subject to currency exchange fluctuations and high transfer fees.

Blockchain plays an important role in cross-border money transfers by introducing stablecoins and digital currencies that enable quick payments. Additionally, it facilitates speedy settlements without relying on the SWIFT network and considerably lowers transaction fees.

- Digital Identity Management & KYC

KYC is a time-consuming but critical procedure for banking institutions that includes gathering valid ID proof, dealing with documentation checks, biometric verification, and much more. It can take several weeks to verify users and demand significant resources as well.

However, blockchain allows banks to streamline the KYC process by recording complete customer identities and transaction histories. It makes it simpler to track the transactions and validate these user identities. Consequently, the implementation of blockchain technology reduces the likelihood of fraud and maintains regulatory compliance.

- Smart Contracts for Automation

Smart contracts allow banking institutions to automatically enforce the terms of their confidential contracts without any human intervention. These self-executing digital agreements can be configured to initiate banking operations (like payment processing) that follow predetermined protocols.

- Fraud Detection and AML

Blockchain creates a transparent and immutable record of transactions, making it easier for financial institutions to comply with AML regulations and even carry verifiable audit trails. It also supports real-time transaction monitoring for detecting suspicious activity and flagging any anomalies in the operations.

- Asset Tokenization

Blockchain is opening new avenues of decentralised finance (DeFi) for banks. Decentralised technology converts traditional assets such as stocks, property, bonds, and more into digital tokens. A distributed ledger records these tokenized assets, ensuring secure and efficient transferability while maintaining their real-world value. Moreover, advanced practices like fractional ownership allow investors to own a portion of high-value assets. This approach improves asset accessibility, liquidity, and market participation for banks.

- Fundraising

Banking institutions can utilise Security Token Offerings (STOs), Initial Coin Offerings (ICOs), and other advanced fundraising mechanisms. These models have emerged as a result of blockchain technology and can fund new bank ventures while maintaining transparency and enhancing investor trust.

- Loan and Credit Approval

Customers often express frustration with the lengthy loan and credit approval procedures. But there isn’t much to blame financial institutions for because these verification processes are multifaceted and complex.

Blockchain technology enhances the speed and efficiency of these procedures by offering decentralised identity verification. Blockchain stores data in a distributed ledger, allowing banks to perform real-time analysis of a borrower’s financial status.

- Trade Finance

Banks can use blockchain in trade finance to replace traditional, paper-based systems with secure, immutable digital data. This not only simplifies transaction record-keeping but also increases transparency and efficiency in letter-of-credit processes.

Challenges and Considerations For Blockchain Adoption In Banking

There are several advantages and applications of blockchain adoption, but it presents some challenges, such as:

- Banking is a highly regulated industry, but there are still significant uncertainties surrounding blockchain and cryptocurrency, which complicate compliance.

- There has been a slight rise in phishing scams, identity theft, hacking, and other security-related challenges for banks with blockchain adoption.

- Banks have highly complex and outdated legacy systems, which are often incompatible with blockchain solutions.

- Banks handle several transactions simultaneously, but public blockchain solutions occasionally have latency and throughput issues. It could impact transaction speed, especially during heavy traffic hours for banks.

Conclusion

Blockchain is benefiting the banks with sophisticated features, making digital payments more secure, speedy, cost-efficient, and transparent. As this technology continues to evolve, we can expect further advancements in the banking sector as well, with increased adoption of blockchain.

Leading blockchain development companies, such as Webcom Systems, are helping banking institutions integrate blockchain capabilities into their traditional systems and promote digital transformation. With secure and quick blockchain-powered payments, banks can operate more smoothly and offer better services to their customers.

Also Read: Artificial Intelligence and Blockchain Integration In Business

Related Posts

Webcom Systems Pty Ltd is a technology development and consulting company that builds blockchain, Web3, digital currency, NFT, DeFi, remittance, and related software solutions. Our role is strictly limited to providing software development, technical architecture, and strategic consulting services. We do not provide financial, investment, brokerage, exchange, asset management, taxation, legal, or trading services to businesses or individuals. We do not operate financial institutions, manage client funds, execute trading operations on behalf of users, or offer investment, tax, or legal advice of any kind.

Any legal compliance, license, regulatory approval, government registration, permit, KYC/AML implementation, and any other statutory obligation must be obtained and managed entirely by the client. Webcom Systems Pty Ltd does not assist in obtaining licenses or regulatory approvals from any authority.

All information provided on our website, marketing materials, proposals, and communications is for general informational purposes and does not contain investment, legal, or financial advice specific to you. You may rely on this information strictly at your own risk. No particular piece of information issued by us constitutes a proposal or request for a proposal to invest. We do not recommend, endorse, or sponsor any assets, securities, companies, or funds.

Clients are entirely responsible for conducting independent due diligence and are professionally advised to seek assistance from licensed financial advisors, legal counsel, and regulatory professionals to make such critical choices. Webcom Systems Pty Ltd accepts no liability for any decisions or financial consequences of your investment decisions.

Risk WarningInvesting and trading in financial markets involve a high level of risk. The value of financial products may fluctuate significantly, and you may lose part or all of your invested capital. It is preferable to fully comprehend how different financial products work before making any investment decisions. You should also carefully evaluate your financial situation, investment goals, and risk tolerance, and consider all risks involved before investing.

Error: Contact form not found.